Life Sciences

Tale of Two Stories: Growth is Uneven

Precision Beats Expansion When Growth Is Uneven

When growth diverges, expansion creates waste. Precision creates results. In Q2 planning cycles, commercial leaders are shifting their thinking from “How do we add or deploy coverage?” to “What type of coverage converts?”

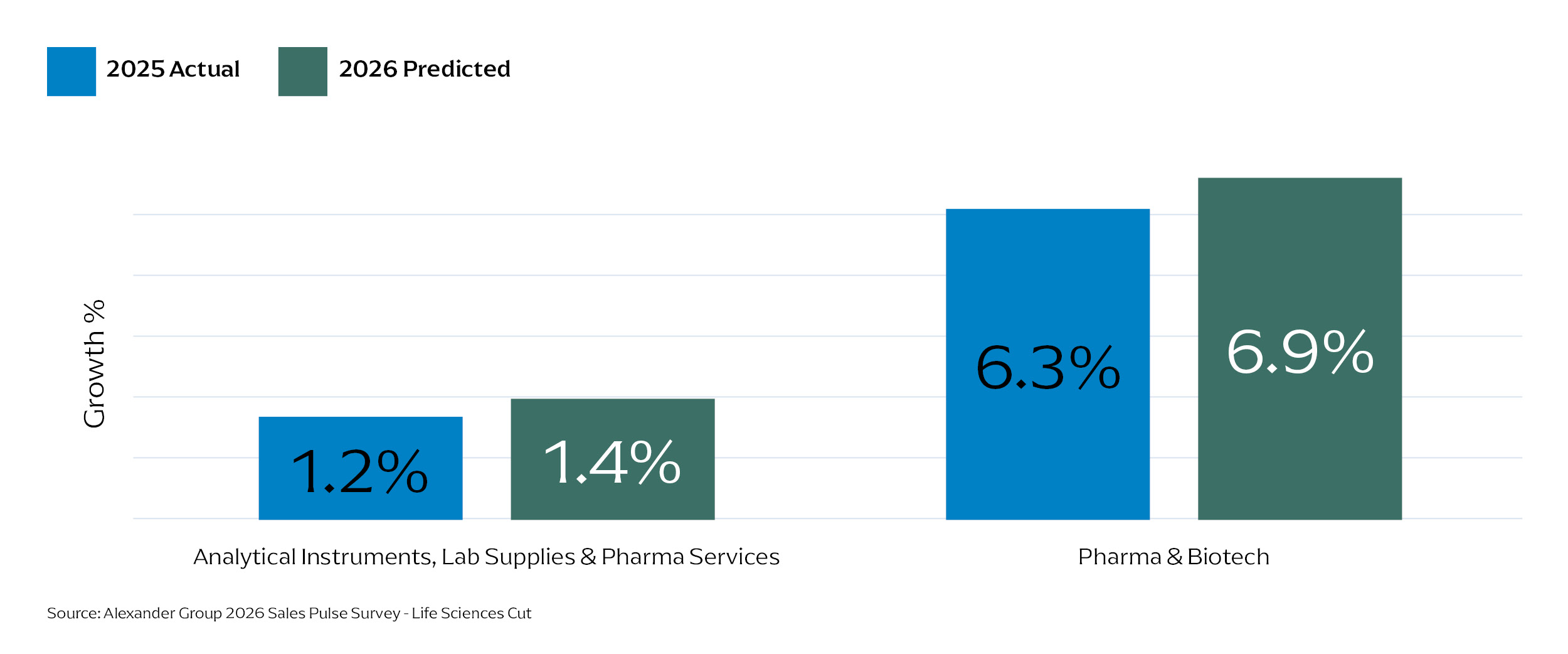

The revenue outlook stays steadier in pharma and biotech: Our survey shows 6.3% actual growth in 2025 and 6.9% expected growth in 2026. However, analytical instruments, lab supplies and pharma services tell a different story: 1.2% actual growth in 2025 and 1.4% expected in 2026. That gap changes what good looks like in coverage, incentives and operating cadence.

Averages hide the problem. Blended growth assumptions mask volatility, delay course correction and let underperformance compound until it becomes the new baseline.

Precision forces hard decisions earlier before the quarter forces them for you:

- Which segments still earn high-touch coverage at today’s cost?

- Where does growth justify a specialist and a seller team, and where should you go lower-touch?

- Which accounts need proactive protection, and which should you pursue opportunistically?

The Q2 implication that leaders shouldn’t wait for a macro-rebound. Instead, reallocate effort to segments and accounts where you can win now and stop funding motions that don’t convert.

Coverage Models Must Earn Their Cost

Sales still represent the biggest commercial bet, and leaders are doubling down. In analytical instruments and pharma services, 62% of companies plan to increase sales investment in 2026 (with marketing and service close behind at ~39% each). The point is to make every dollar and every role earn its keep.

Field sellers still matter, especially in complex therapeutic conversations and high-value instrument deals. However, the operating model bleeds out time. In time studies, sellers often spend ~50% of the week on non-customer-facing work. And when they do get into the market, many default to familiar accounts and products instead of expanding coverage across the buying group.

Rather than responding with slogans, leaders are turning to redesign. Across segments, three structural shifts keep coming up:

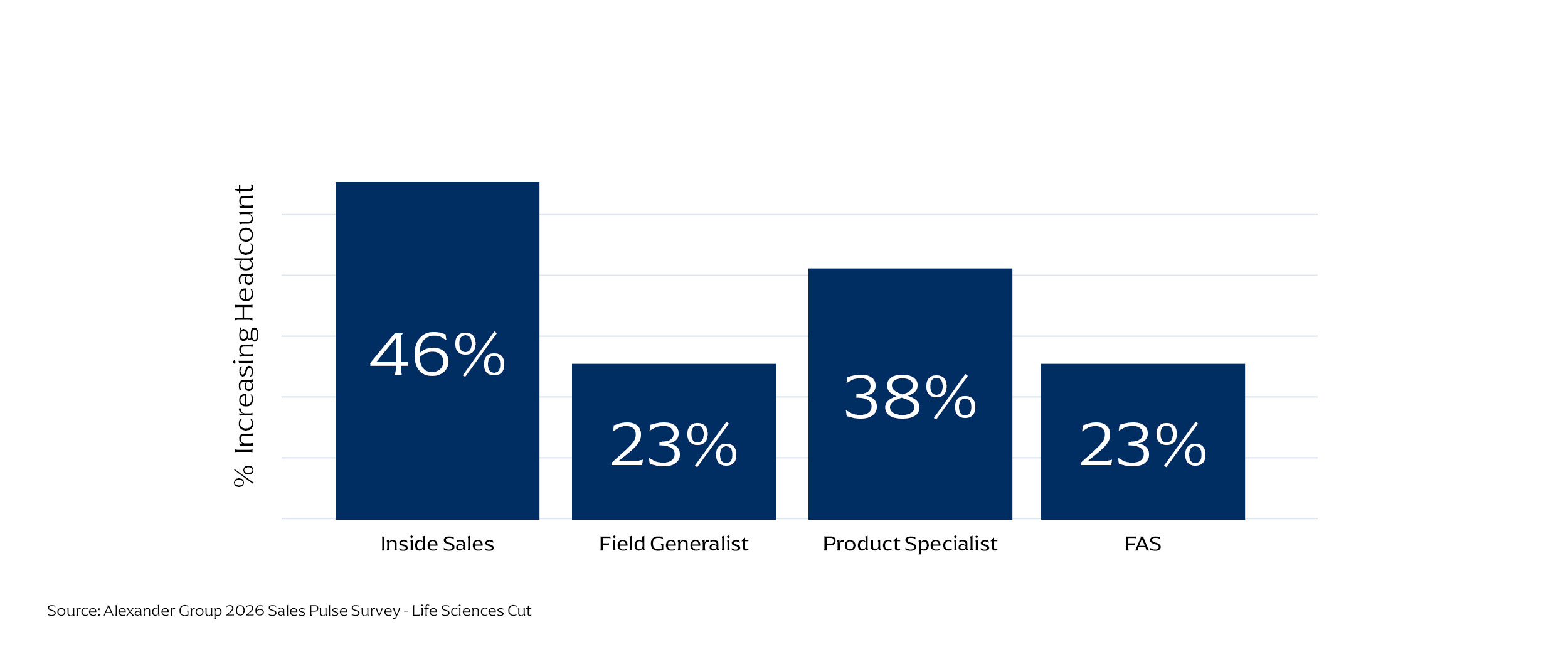

1) Inside sales keeps rising, but it doesn’t win everywhere. In analytical instruments and pharma services, 46% of companies plan to increase inside sales headcount. Inside sales performs best in recurring, consumable-oriented models and when it augments field sellers. When teams try to use inside sales as a drop-in replacement for complex capital selling without the enablement, tools and coverage design to match, that’s when companies see underperformance

2) Coverage is specializing because buyers demand depth. Companies are moving away from the one-size-fits-all seller. Instead, they’re building coordinated teams of account managers, product specialists and technical experts (often including Field Application Specialists (FAS)) supported by inside sales. That shift reflects what customers reward: continuity and technical credibility, which is especially important as growth comes from share gain, not broad market expansion.

3) The long tail is going digital—and fast. More demand is moving to automated, self-serve or distributor-led motions. That shift can lower cost-to-serve, but it also compresses differentiation. Channel partners are pushing buyers to digital self-service, so suppliers who “just hand it to channel” risk getting disintermediated and losing the customer data flywheel.

Capacity without focus amplifies drag, so treat coverage like an operating system: instrument it, tune it and hold each role accountable for measurable contribution.

Productivity Is a System Problem, Not a Seller Problem

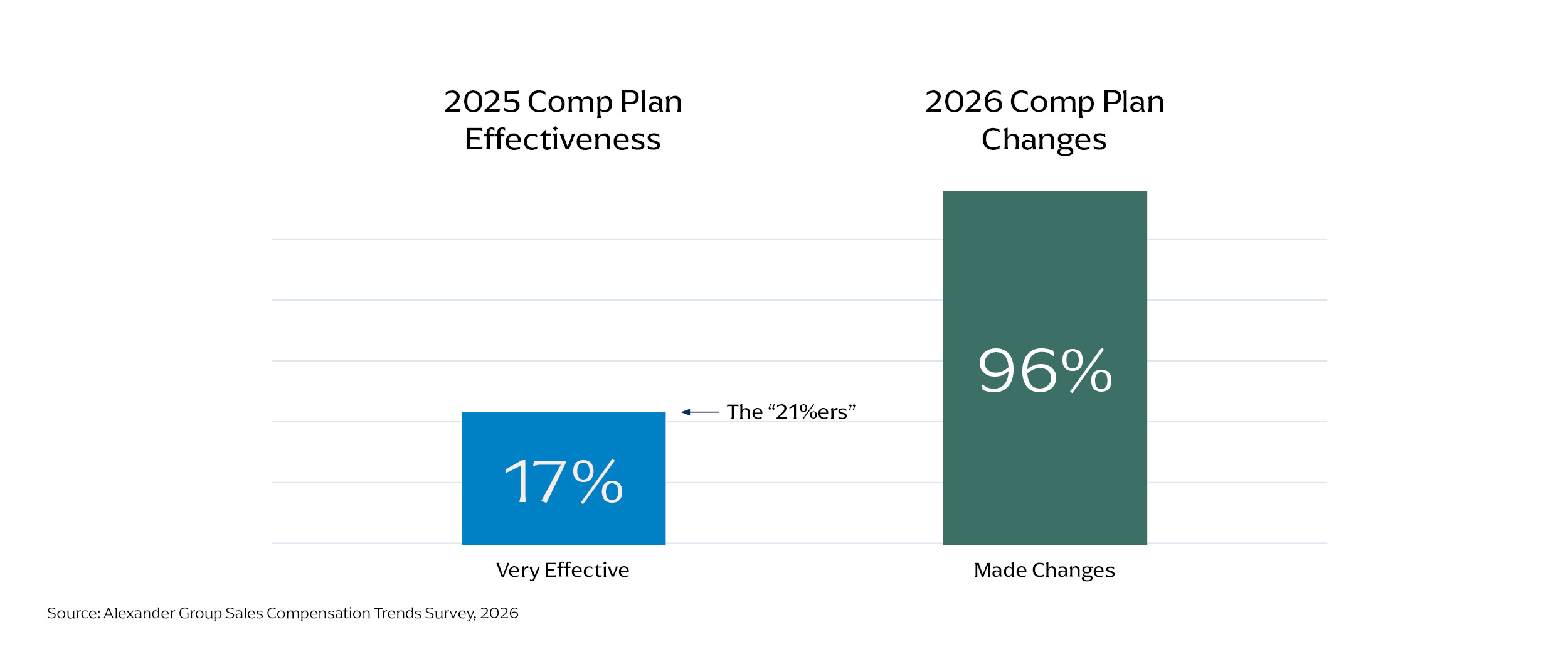

The best companies choose to redesign the system, as opposed to how lower-performing companies squeeze sellers hard. In our research, only about one in five companies rate their sales compensation plans as very effective (the 21%ers), yet they outperform peers on revenue and quota attainment without materially higher incentive spend.

Productivity is an operating system issue: Roles, processes, tools and incentives either remove friction or create it. Our survey shows that this pressure is landing everywhere: Nearly every company is reworking how they pay and manage performance in 2026.

What separates the top performers is discipline, not a richer payout. The “21%ers” tend to do four things well:

- Tie incentive measures directly to the growth strategy you’re pursuing

- Set quotas that stretch but don’t break confidence

- Run tight governance across Sales, Finance, HR, Marketing and Compliance

- Operate the program year-round with a clear cadence and crisp communication

Quota design is still the hardest part, and that shows up fast in attrition and effort. When fewer than half of sellers hit quota, voluntary turnover climbs and performance distribution compresses. When targets align from corporate guidance to the field, sellers trust the plan, managers coach to it and discretionary effort follows.

In Q2, treat incentives like an execution lever instead of an annual artifact. With 96% of companies changing 2026 sales compensation plans, the bar is rising on speed, clarity and governance. Teams that connect measures to strategy and run a tight operating cadence will move faster than teams that set it and forget it.

AI Delivers Value Only When Tied to Execution

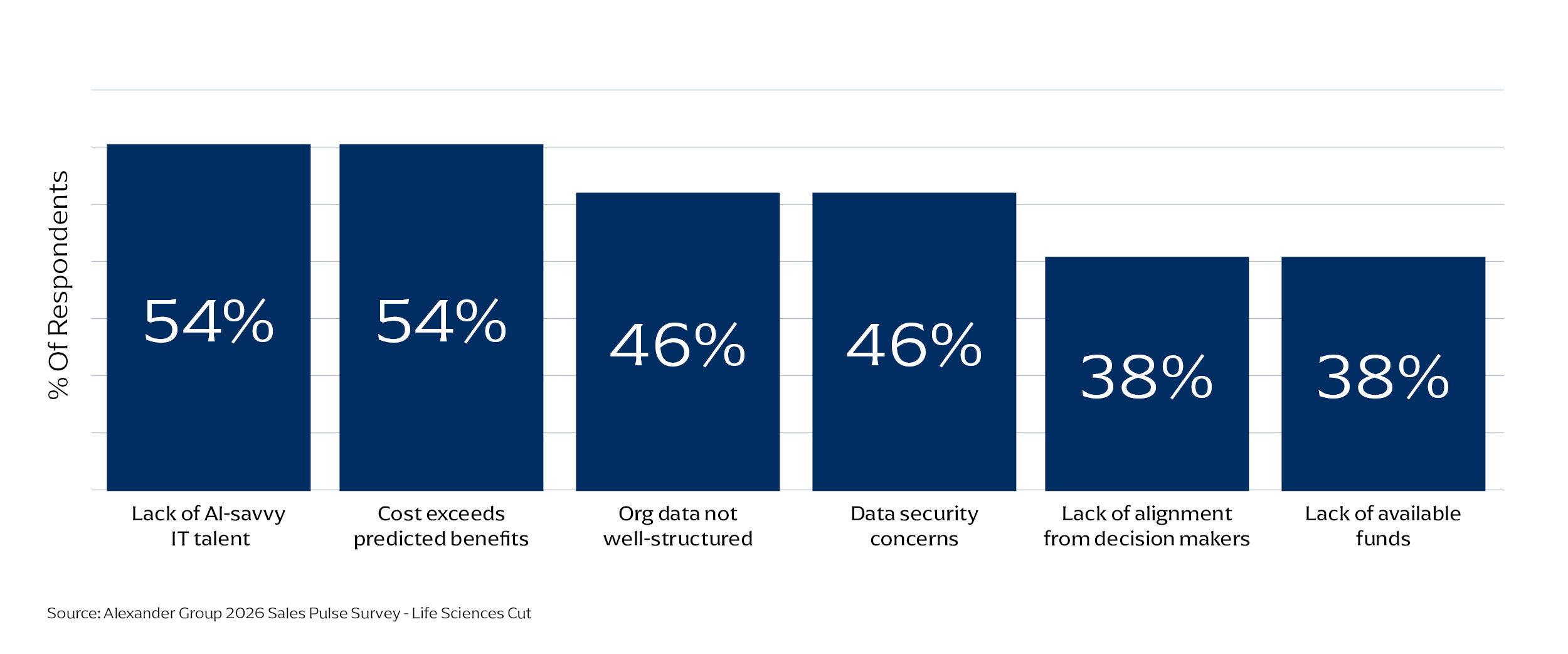

AI is now on almost every commercial roadmap, but leaders are treating it as an execution tool when they should be treating it as a science project. In the Sales Pulse Survey, the top blockers are practical constraints like a lack of AI-savvy talent and uncertain ROI (both cited by ~54% of respondents), followed by data readiness and security concerns (each ~46%).

Teams that struggle to prove ROI tend to start with enterprise-wide transformation programs. Although those programs add vendors, workflows, and governance, they rarely change what sellers do on Monday morning. Teams that see traction do the opposite by picking a use case tied to execution and scale only after it sticks.

Teams gaining traction also tie AI to specific moments in the workflow. They use it to re-engage dormant prescribers, cut lead prep from days to hours and recommend the next best action so sellers move faster and waste fewer calls.

Two constraints keep showing up, and the survey data reinforces them. First, data readiness: Without clean customer hierarchies and usable data, models and recommendations fall apart. Second, capability: Without AI-savvy talent (a top barrier for ~54% of respondents), adoption stalls. Winning teams build the data foundation and the talent bench before they chase broad automation.

Leaders should take a pragmatic approach: Use AI to protect seller time and sharpen focus. Next, anchor investment in one or two workflows, prove behavior change and then scale. Otherwise, AI becomes another layer of friction instead of a performance advantage.

The Q2 Imperative

Q2 isn’t a waiting room. It’s a sorting mechanism, separating commercial teams that can convert effort into outcomes from those that can’t.

In the slow lane, you win by making the model cheaper to run and easier to execute. In the fast lane, you win by scaling without creating drag. Either way, the playbook is the same: Choose where you’ll be precise; make every role earn its cost; and run incentives, data and AI as weekly execution levers.

If you want one line to steer Q2: Fund the motions that convert and starve the ones that don’t. Momentum rarely “returns.” It gets taken.

- Lock the lane: Segment your book into fast-lane and slow-lane assumptions and plan coverage accordingly

- Instrument execution: Measure where seller time goes and cut the top two sources of non-selling work

- Make levers real: Tune sales compensation measures, enablement, and AI use cases around the behaviors you need this quarter