Getting the Mix and Leverage Right

What is the right mix and leverage for the sales compensation plan?

The sales compensation task force of a major company is now meeting. Let’s listen.

The VP of Sales begins: “We need more push from our salespeople. Maybe our sales compensation plan needs more punch. Maybe the base salaries are too high. Our salespeople need to be hungrier. Let’s move some of the base salary monies to the commission plan.”

The Eastern Area Sales Manager continues: “I agree. Our biggest competitor has a real aggressive incentive plan. Its senior salespeople are big hitters…with the upside paychecks to match. Our plan is just too shallow.”

The Chicago District Manager comments: “Maybe we can keep the base salaries the same but offer more upside earnings. We could add another accelerator for above 130% performance.”

Finally, the business unit manager reflects: “Let’s be careful here. We had low base salaries a couple of years ago. As you will recall, the commission plan had several upside commission accelerator ramps. Remember, we changed the plan: We increased base salaries to provide more stability to earnings…they were too erratic in the past. And don’t forget when two sales reps made more than the CEO. While I might not have agreed with the decision, no one was surprised when we had to reduce the upside accelerators.”

Mix and Leverage

Like most sales compensation task forces, these managers will wonder aloud what the best relationship between base salary and variable pay is for the sales compensation plan. What should it be: low base salaries with high upside earnings potential? Or high base salaries with more modest upside earnings potential?

This is a discussion about the mix and the leverage of the sales compensation plan. Here is our question: What is the right mix and leverage for the sales incentive plan?

Before answering, let’s correctly define mix and leverage. Many of us use the words “mix” and “leverage” as synonyms; they are not.

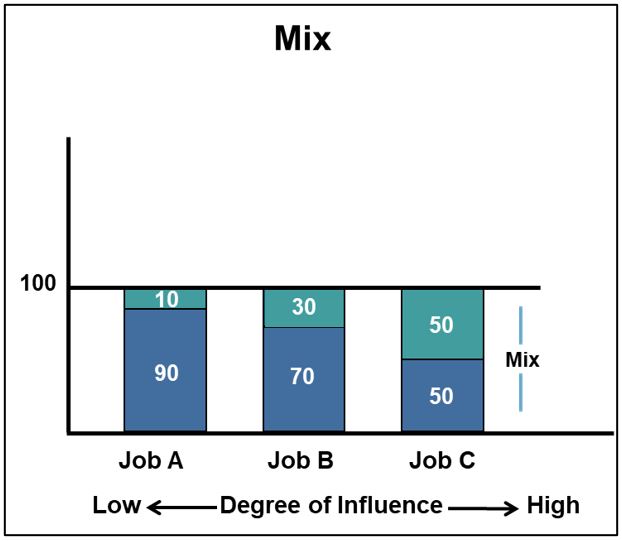

Mix. The mix is the relationship between the base salary and the incentive component of target total compensation (TTC) for expected performance. The mix is expressed as a ratio of two parts of 100% (of TTC). For example, a 70/30 salary mix is a plan that has 70% of the TTC reserved in base salary while 30% of the TTC is the target incentive amount.

Whether we formally recognize it or not, all sales jobs have a target total compensation. This is the amount of pay (both base salary and target incentive earnings) that management wants the average salesperson to earn for achieving expected performance.

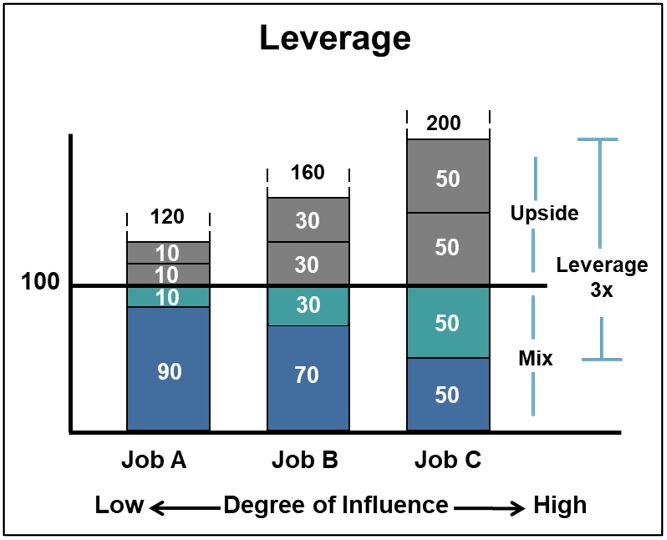

Leverage. Don’t confuse leverage and mix. The leverage is the total amount of incentive monies available for outstanding performance. It is expressed as a multiple of the target incentive amount. For example, a 3x leverage provides 3x the incentive amount for outstanding performance. For a 70/30 mix, the earnings potential of the best performers (90th percentile) is 3 times 30, which equals 90. For a pay plan with a TTC of $100K, the base would be $70K, the target incentive $30K and the outstanding incentive earnings would be $90K. In this scenario, poor performers would earn $70K (base pay only). Average performers (achieving quota) would earn $100K. Best performers could earn $160K. ($70K base pay plus $90K incentive earnings equals $160K).

What about pay caps? Determining the leverage for a sales compensation plan does not address the issue of whether caps should be used. For uncapped plans, the leverage reflects the earnings potential available for the outstanding performers—normally the 90th percentile of sales personnel. In practice, several individuals might exceed this upside target earning level…but, hopefully, not by too much.

A Notion Method

Here is an example of a simple notation method to express both the mix and leverage of an incentive plan: “70/30/3x.” The first two numbers represent the mix: the ratio of base salary and target incentive earnings expressed as two parts of 100%. (Of course, 100% is the planned TTC amount.) The third number—3x—is the leverage of the plan. It means that outstanding performers could earn up to 160% of the TTC level (3 times $30K, added to the base pay of $70K equals $160K). In an uncapped plan, several individuals may pass this upper limit. However, if the formula is designed correctly, the number of salespeople passing this upper leverage amount should be less than 10% of the sales force.

In summary, the mix, expressed as two parts of 100%, describes the ratio between 1) base salary and 2) target incentive earnings as a percent of TTC. The leverage is the amount of monies available for top performers. It’s expressed as a multiple of target incentive.

What is the Right Mix?

Degree of Persuasion

The most important factor affecting the selection of the mix is the degree of persuasion—influence—the seller applies to get the customer to act. The more important the salesperson is to the sale of the product—as compared to other factors such as product features, service/merchandising and price—the more aggressive the pay mix (low base salary/high incentive opportunity).

Use high mix plans when the efforts of individual performers almost exclusively determine the success or failure of a sales effort. Certain jobs, such as the so-called “income producers,” receive relatively low base salaries and high incentive earnings. Income producers create revenue through their individual efforts. Examples include stock, real estate, life insurance, and some distributor sales jobs.

At the other end of the spectrum are sales jobs where the salesperson is one of many factors contributing to the overall sales process. Complex technical selling, long sales cycles, government sales, and branded products sales all need sales support, but selling is only one factor in the buying decision. A degree of persuasion still exists in these jobs, but it is less aggressive than, for example, income producers.

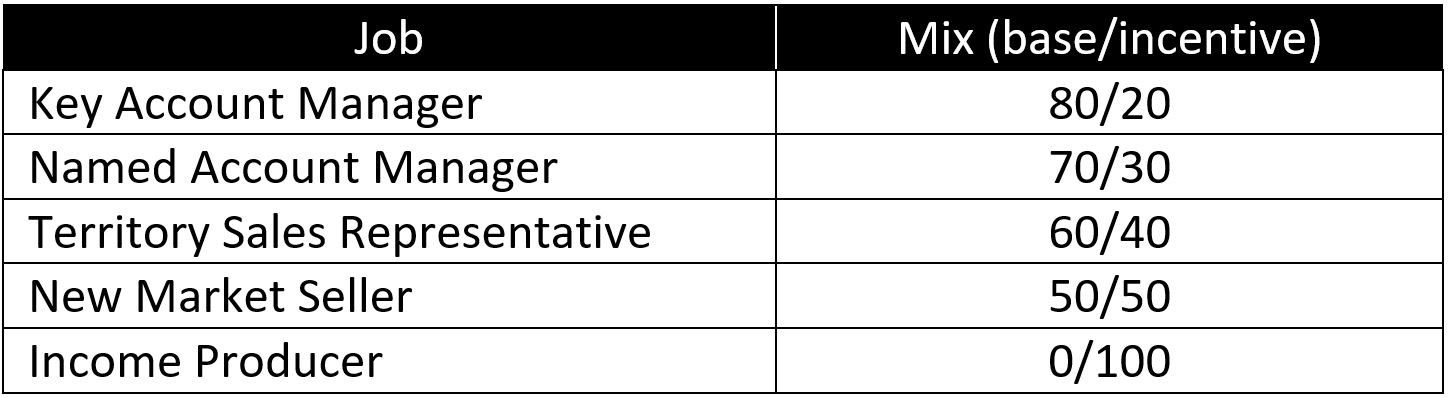

Here are some typical pay mix examples found for different types of direct sales jobs. Note, these mixes often vary by industry.

Incentive plan designers can assess the degree of persuasion for a job by examining several factors. The more distinct the product, the longer the sales cycle, and the need for a group sales effort will justify a more modest pay mix with a higher base pay and a lower incentive amount. Also, if quota setting is inaccurate or performance difficult to measure, you may need to select a lower mix—more base salary, less incentive.

Picking the right mix will significantly affect the impact of the incentive plan. The mix is something akin to a thermostat. The higher the mix (the more money “at risk”), the more likely the salesperson will be driven by the incentive plan, sometimes to the exclusion of other factors. A high mix plan tells the salesperson that the performance measures in the sales incentive plan are extremely important. In fact, a high mix plan almost encourages the salesperson to put on blinders. Sales personnel who are driven by the sales compensation program may ignore objectives and direction provided outside the sales compensation plan.

On the other hand, a low mix plan (high base salary) signals the relatively low importance of the sales compensation plan. Consequently, a low mix plan will allow the salesperson to be more attentive to direction provided through other means such as supervision, training and procedures.

What to Avoid When Determining the Mix

Many managers cast about looking for a rationale to select the proper mix. As mentioned above, the content of the sales job determines the degree of mix. However, here are several factors that managers let influence the selection of the mix leverage, but they should not.

What Others Do. This should be the least important factor to affect the selection of mix. Yes, be competitive with the TTC levels of other companies, but let the content of your jobs, not theirs, determine the mix of your sales compensation plan.

Variable Cost Management. Some believe that keeping the base salaries low helps keep costs variable. Be careful. An effective sales organization cannot withstand deep swings in sales compensation earnings, particularly if the swings are caused by economic patterns and not by individual sales efforts. The true cost of such high mix plans will be registered in the form of high turnover. For most sales organizations, high turnover can negatively affect market position, training and recruitment costs.

Old Adage Theories. Avoid these old adages: “Put a lot of pay at risk…then see them work!” Or “Give them a high base salary, they will be loyal to us like no one else!” Interesting observations, but not useful when selecting the mix. People seek alignment among the various elements in their job world. The mix should match the nature of the job and its relative importance in the sales management process.

The selection of the mix should be driven by the nature of the job and not by factors such as what others do, variable cost considerations or old adages.

What is the Right Leverage?

Designing the payout formula for the upside earnings—over TTC—is critical to the success of the pay program. Better performers should earn distinguished rewards for outstanding performance. But how high is high? Many would argue that salespeople should have no limit to their upside earnings. Maybe yes, maybe no. Regardless, the upside earnings target still needs to be identified. Otherwise, the plan may pay too little, or too much.

The proper method to establish a target level of pay for outstanding performance is to use compensation survey data to identify the target level of pay for your best performers. Generally, the upper 10th percentile performers should earn at the upper 10th percentile of the labor market for similar jobs. You may want to pay more or less, but you should not be at a significant advantage or disadvantage to the labor market. Of course, if the plan is uncapped, then expect some sales personnel to exceed this target upper amount.

A Shortcut: The 3x Leverage Rule

After examining extensive amounts of survey data, a pattern has emerged that may help you initially identify the leverage for the plan.

The compensation survey data suggests that the amount of upside earnings is related to the downside risks, on a “2-for-1” ratio; or 3x the at-risk component. That is, for every dollar of TTC put at risk, two dollars of upside earning potential are provided for outstanding performance. As a result, the more money at risk (high mix), more upside earning opportunities should be available.

Again, this 3x rule does not suggest a cap. Instead, it identifies where the upper 10th percentile of performers should be paid—the 90th percentile. Some might exceed this amount.

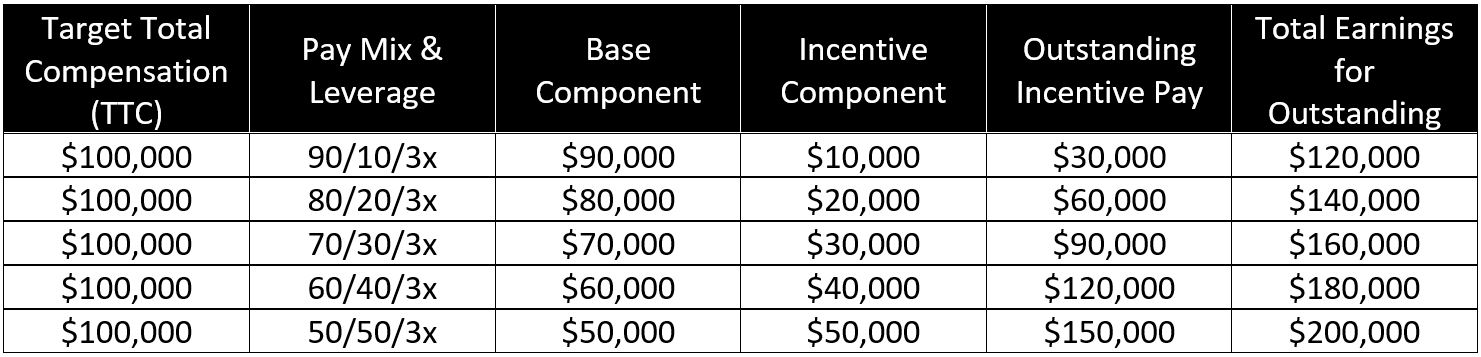

Let’s see how this 3x rule works. Let’s assume we have a direct salesperson with a $2M territory. Using market data and adjusted for the company’s pay philosophy, we have identified the TTC of $100K. Here are how the various mixes would affect base salary and upside earnings potential.

Notice that more upside earnings become available as the mix increases on a 2-for-1 ratio. For example, in the 90/10/3x plan, the at-risk money is $10,000; the upside allows an additional $20K over TTC of $100K. This provides theoretical upside potential earnings of $120K. The $20K is twice the $10K, thus fulfilling the “2-for-1” ratio. The $10K (at target) plus the $20K for over target performance added together provide a total of $30K; 3x the $10K. Now, examine the pay plan with a 50/50 pay mix and the same 3x leverage. Using the same TTC, the total upside earning opportunity (with base pay) would be $200K. ($50K times 3—$150K added to the base of $50K equals $200K for the best performers) Of course, the 3x leverage amount is an estimate of the 90th percentile in the labor market. Confirm this amount with survey data.

Remarks

The selection of mix and leverage is one of many critical steps necessary to develop an effective sales compensation plan. Also important is 1) establishing TTC, 2) selecting performance measures, 3) identifying the correct formula type (commission, bonus or both), and 4) timing-measurement periods and payout dates. However, starting with the proper mix and leverage will significantly ease the design process.

The ‘False’ High Mix Plan

As you start to pencil out the elements of your plan’s mix and leverage, you may notice something out of sync. You may have a very aggressive mix—such as a 50/50 plan. But your upside earnings may be a lot less than the suggested 3x leverage already described.

What gives here?

Don’t worry, your plan is probably fine. Some plans have shallow upside earnings potential. Why? To avoid overselling the factory, to control unreasonable costs or to limit the impact of windfalls. Additionally, your labor market may not have a 3x leverage but instead a 2.5x, 2x, or even a 3.5x.

However, there may be another reason why you have a shallow upside potential even with an aggressive pay mix.

Some companies have legacy sales incentive plans from their start-up days. These outdated high mix plans are no longer relevant to the sales process, yet sales management still uses them. Unfortunately, the upside potential amounts get “shaved down” as the required degree of personal sales persuasion declines relative to other influencing factors. The customers no longer buy because of the consequential sales efforts of an individual salesperson. Instead, it’s the product, its proven utility and professional level of after-the-sale customer service that now cause the customer to buy.

Test your “high mix” plan. How much of the at-risk money is really on the line? You may find that your 50/50 plan is really a 70/30 or 80/20 plan. Repeat business could now account for a large portion of the sales dollars. The salesperson, with minimal effort, is almost assured 70% to 80% of their TTC earnings. Thus, your 50/50 plan is really a myth. If this is the case, maybe it’s time to officially recognize some of these monies in the base salary program.

Get Mix and Leverage For Sales Compensation Plans Right

To explore customized solutions and to learn more about effective sales compensation planning, contact us and speak with our experts!